Blog

Joint account in the Philippines: how having one may affect your deposit insurance coverage

A joint time deposit lets two or more people share ownership of a single fixed-term account. One person opens and manages it, while the rest are invited as co-holders and have viewing access. This article explains how it works at Salmon Bank (Rural Bank) and how PDIC deposit insurance applies.

What is a joint account?

A joint account is a deposit account held in the names of two or more people. Each person named on the account is a co-owner of the deposit. For insurance purposes, PDIC treats a joint account separately from any individual account the same person holds at the same bank.

At Salmon Bank (Rural Bank), joint accounts are available for time deposits. One person opens the account as the primary holder and invites up to nine co-owners, for a maximum of ten holders in total. The primary holder controls the account, while co-holders have viewing access.

A joint account is not the same as naming a beneficiary. Co-holders are actual co-owners of the deposit from the moment they accept the invitation and sign the agreement.

What is PDIC deposit insurance?

PDIC, the Philippine Deposit Insurance Corporation, is the government agency responsible for bank deposit insurance in the Philippines. All deposits in PDIC-member banks are covered in accordance with applicable PDIC rules and regulations.

Since March 15, 2025, the PDIC insurance limit is ₱1,000,000 per depositor per bank. This applies to PDIC insured deposits in member banks, including savings, time, and demand accounts. Salmon Bank (Rural Bank) is a BSP-licensed, PDIC-member institution.

Keep in mind that this PDIC limit applies per depositor, not per account. Even if you hold multiple accounts at the same bank, your total PDIC insurance coverage across all of them is still subject to the ₱1,000,000 limit.

PDIC deposit insurance applies to eligible deposits in PDIC-member banks, subject to PDIC rules and limits. It does not apply to losses from fraud, scams, or unauthorized transactions. Not all deposit-taking institutions are PDIC members, so check your bank’s membership status before opening an account.

How a joint account may affect your PDIC insurance coverage

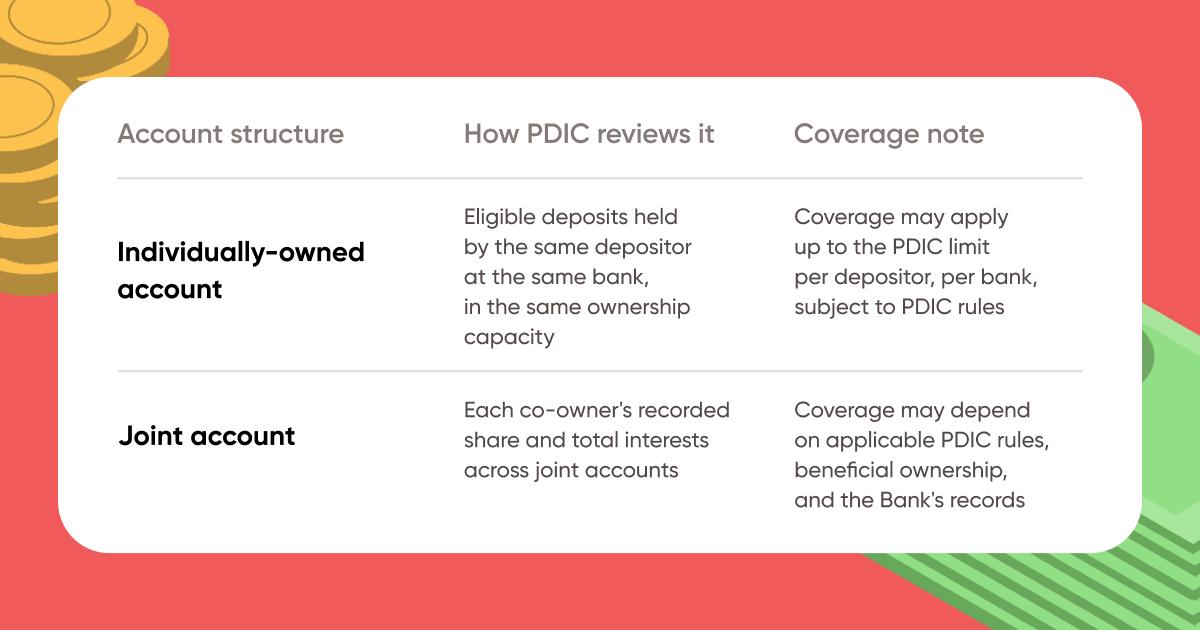

Under Section 5(k) of the PDIC Charter, a joint account is treated separately from any individually-owned account for insurance purposes. This is where the distinction becomes important.

For joint accounts, PDIC coverage may apply to each co-owner’s recorded share separately, subject to applicable PDIC rules, beneficial ownership, and the Bank’s records. The PDIC limit still applies per depositor, per bank, and each co-owner’s interests across joint accounts may be added together when coverage is calculated.

Keep in mind that a person’s total recorded interests across joint accounts in the same bank remain subject to the standard ₱1,000,000 PDIC coverage limit. If you hold multiple joint accounts at the same bank, your combined recorded interests across those accounts may be taken into account.

The following examples are for illustration only. They are not advice to split, arrange, or structure deposits for insurance coverage. Actual PDIC coverage depends on applicable PDIC rules, beneficial ownership, and the Bank’s records.

Subject to applicable PDIC rules, beneficial ownership, and the Bank’s records. Each co-owner’s total recorded interests across joint accounts at the same bank remain subject to the ₱1,000,000 PDIC coverage limit.

In an individually-owned account, PDIC considers the depositor’s eligible deposits at the same bank and in the same ownership capacity. Coverage remains subject to the ₱1,000,000 limit.

In a joint account, PDIC may review the account separately from individually-owned deposits. Coverage may depend on each co-owner’s recorded share, aggregate interests across joint accounts, beneficial ownership, applicable PDIC rules, and the Bank’s records.

The PDIC’s own illustrative cases on joint accounts provide further guidance on how coverage is calculated.

Who this is relevant for

A joint account may be relevant for customers who want to understand how holding a deposit jointly may affect PDIC deposit insurance coverage at the same bank, subject to PDIC rules. Here are some situations where a joint account may be worth considering:

Partners or family members placing money in a shared time deposit, where each person’s ownership share may be reflected in the Bank’s records

People who want to better understand how deposit insurance may apply to deposits held jointly at Salmon Bank (Rural Bank)

Anyone who wants a co-holder to have visibility over a deposit account without giving them full account control

This works well for time deposits, where money earns interest over a fixed term while ownership and account visibility remain clear.

How a joint account is managed

In a Salmon Bank (Rural Bank) joint time deposit, one person starts as the primary holder and manages the account. This includes opening the account, inviting co-holders, updating settings, and closing the account when needed.

The primary holder can add co-holders, who then become co-owners of the deposit. Co-holders have viewing access and can check the balance, see transaction history, and receive updates. They do not make transactions or manage the account. Co-holders also cannot leave the account on their own.

PDIC treatment may apply to each co-holder’s recorded share separately, subject to applicable PDIC rules and the Bank’s records.

How to open a joint time deposit with Salmon Bank (Rural Bank)

Salmon Bank (Rural Bank) is a BSP-licensed bank that has been serving Filipinos since 1963. It is a subsidiary of Salmon Group Ltd and offers time deposits with terms from 6 months up to 5 years, earning up to 8% interest per year. Minimum deposit starts at ₱5,000.

To get started, fill out the application form on the Salmon Bank (Rural Bank) website or open the Salmon app and start a new time deposit. Our Relationship Manager will then walk you through the rest of the process, including helping you set up your account for you and your co-holders.

Take note that:

Joint time deposits are available with up to 10 holders per account: one primary holder and up to nine co-holders

The joint account feature applies to new time deposits only

Existing time deposits cannot be converted to a joint account

If you prefer to open a joint account in person, you may also visit the Salmon Bank (Rural Bank) branches in Sta. Rosa, Laguna or Bacoor, Cavite.

Open a joint time deposit with Salmon Bank (Rural Bank). Earn up to 8% p.a. on eligible time deposits with terms from 6 months to 5 years. Salmon Bank (Rural Bank) is BSP-licensed and a PDIC-member bank. Open an account

Frequently asked questions (FAQs)

Is a co-holder the same as a beneficiary?

No, a co-holder becomes one of the owners of the joint time deposit after accepting the invitation and signing the required agreement. This is different from naming a beneficiary.

How many people can be part of a joint time deposit?

A Salmon Bank (Rural Bank) joint time deposit can have 2 to 10 account owners in total: one primary holder and up to nine co-holders.

Can co-holders manage, withdraw, or close the time deposit?

No, the primary holder manages the account. Co-holders can view the account and related details, but they cannot fund, close, pre-terminate, update settings, or change payout instructions in the Salmon app.

How are ownership shares divided?

For Salmon Bank (Rural Bank) joint time deposits, ownership shares are equal among all account owners. For example, if there are two account owners, each owner has a 50% share.PDIC treatment may still depend on applicable PDIC rules, beneficial ownership, and the Bank’s records.

Will co-holders receive the payout directly from Salmon?

No, as when the time deposit matures, the proceeds are credited to the primary holder’s Salmon Checking Account. Co-holders should coordinate with the primary holder regarding their share of the payout.

Can a co-holder leave or be removed after accepting?

This is not available in the Salmon app after the invitation has been accepted and the Joint Account Agreement has been signed. If you need help, you may contact Salmon Customer Service via in-app chat.

Does the interest rate change when a time deposit becomes joint?

No, the account remains the same time deposit with the same terms and interest rate. Only the ownership type changes.

07.06.2026