Blog

What Is a Checking Account? Meaning, Uses, and How It Works

If you regularly make important payments, a checking account can help you keep that money separate and ready to use. Instead of withdrawing cash each time, you can pay through checks, a debit card, online banking, or other payment options your bank offers. It also gives you a clear record of your payments, which can be useful for personal finances or business transactions.

The checking account definition is simple: it is a bank account designed for money you plan to spend soon. While a savings account is mainly for money you want to keep, a checking account is for money you've already set aside for payments, withdrawals, and other day-to-day transactions.

If you're in the Philippines, you may consider a checking account if you need to pay by check for rent, tuition, supplier payments, business expenses, or loan payments. It can also help you stay organized when you have regular or higher-value payments to manage.

What is a checking account?

The simple checking account definition is this: it is a deposit account that lets you access your money for regular payments and withdrawals. You can put money in, take money out, write checks, and make payments if the account includes those features.

The checking account you open may come with a checkbook. It may also include a debit card (and ATM access), online banking features, and account statements.

If you are comparing types of accounts, remember that a checking account is different from a savings account. A savings account is usually for keeping money and earning interest, if the account offers it, while a checking account is mainly for payments and withdrawals.

Take note that your bank may also call a checking account a current account. The idea is the same. It’s an account that lets you access money when you need to pay or withdraw.

How does a checking account work?

A checking account works by holding your money and recording every deposit, withdrawal, payment, and transfer. When you deposit cash, receive a transfer, or deposit a check, your balance goes up. When you issue a check, withdraw cash, use a debit card, or send a transfer, your balance goes down.

Before you issue a check or make a payment, check your available balance. The bank may process a check earlier than you expect. A debit card transaction may also reduce your balance right away. If there is not enough money in your account, the bank may reject the payment and charge a fee.

It helps to review your transactions through online banking or account statements. Keep track of checks you have issued, especially if the bank has not processed them yet.

Deposits, withdrawals, and payments

Deposits are money going into your account. These may include cash deposits, bank transfers, check deposits, salary crediting, or other money sent directly to your account if your bank and employer support it.

Withdrawals are money taken out of your account. You may withdraw through an ATM, over the counter at a branch, a check, a debit card transaction, or an online transfer.

You may pay by check, debit card, online transfer, or another payment method your bank allows.

Debit cards, checks, and online banking

A debit card lets you spend or withdraw money from your account, and it uses money already in your account, so it is different from borrowing.

A check, however, is a written instruction to the bank. It tells the bank to pay a certain amount from your account to the person or business written on the check. The person or business receiving the payment is called the payee, while the person issuing the check is called the payor.

Online banking helps you review your balance, check recent transactions, transfer money, and download statements. It can also help you spot any suspicious activity quickly.

What can you do with a checking account?

You can use it for payments that need checks, or when you want a clear record of what you paid and when.

For everyday use, a checking account can help you pay rent, tuition, association dues, loan payments, insurance, or other regular bills. Some landlords, schools, lenders, or service providers may ask for checks, including post-dated checks. A post-dated check is a check written with a future date.

If you run a business, a checking account can help you pay suppliers, receive payments, keep your business money separate from your personal money, and track your transactions more easily.

A checking account does not automatically build credit. It is also not ideal for long-term savings, especially if it earns little or no interest.

Common types of checking accounts

Not all checking accounts work the same. Some are for personal payments. Others are for business use, higher balances, or customers who need more account features.

A personal checking account may help you pay rent, tuition, loan payments, or other regular expenses. A business checking account can help you separate business income and expenses from personal funds.

Some banks offer checking accounts that you can manage mainly online. Others require branch visits for account opening, checkbook requests, or certain updates.

Personal, online, and interest checking accounts

An online checking account lets you manage many account activities through online banking or an app. Before choosing one, check whether it still gives you the features you need, such as checkbook access, statements, support, and ways to deposit or withdraw money.

An interest checking account may earn interest while still allowing payments and withdrawals. Your bank may require a higher balance before the account earns interest or avoids fees.

Checking account fees and maintaining balance

Before you open a checking account, check how much it may cost to keep and use. The maintaining balance and fees can affect whether the account is practical for you.

The maintaining balance is the minimum amount your bank expects you to keep in the account. Some banks use average daily balance. This means the bank looks at your balance across a period, not just your balance on a single day. If your balance falls below the required amount, the bank may charge a fee.

Common fees may include monthly service fees, below-balance fees, checkbook fees, stop payment fees, ATM fees, transfer fees, statement request fees, and dormancy fees. The bank may charge a dormancy fee if your account has no activity for a long time.

If you see an account described as a free checking account, check what “free” covers. Other fees may still apply. If you are comparing accounts by the lowest maintaining balance, also check the checkbook cost, online access, and support.

How to open a checking account

Before getting your documents ready, think about how you plan to use the account, including whether you need checks for rent, a checkbook for business payments, access to online banking, a debit card, or a branch.

Once you know what you need the account for, compare the initial deposit, maintaining balance, fees, checkbook access, debit card access, online banking features, and how you can get help if needed.

The bank will usually ask you to complete an application form, submit documents, verify your identity, provide specimen signatures, and make the required initial deposit. A specimen signature is the official sample signature the bank uses to check signed documents or checks.

Some banks may let you start your application online. Others may require a branch visit. Banks can change their requirements, so check the bank’s website or app, or ask at a branch before preparing your documents.

Requirements for a checking account

Checking account requirements vary by bank, but you might usually need:

A valid government-issued ID

Contact details and address information

A recent photo or selfie verification, if required

An initial deposit

Specimen signature cards

Tax information or other customer details required by the bank

Business documents, if you are opening a business account

If you are opening a business account, the bank may ask for registration papers, permits, board resolutions, or documents naming the authorized signatories.

When do you need a checking account in the Philippines?

In the Philippines, a checking account is usually not for small day-to-day expenses. Many of those payments can already be handled through bank transfers, e-wallets, debit cards, or QR payments.

A checking account becomes more useful when you need to pay by check or issue post-dated checks. This may apply to rent, tuition, supplier payments, business expenses, loan payments, or other payments where the person or business asks for checks.

It can also help when you want a clearer record for bigger or recurring payments. Each check you issue creates a record of who you paid, how much you paid, and when the check was processed.

Before opening one, ask whether you really need check payments. Then compare the maintaining balance, fees, checkbook cost, online banking access, requirements, and how the bank handles returned checks.

Is a checking account the same as a bank account?

A checking account is a type of bank account. But not every bank account is a checking account. A bank account is a general term. It can refer to different types of accounts, such as a savings, checking, payroll, business account, time deposit, or other financial products.

A checking account is more specific. It is mainly for payments, checks, withdrawals, transfers, and regular transactions.

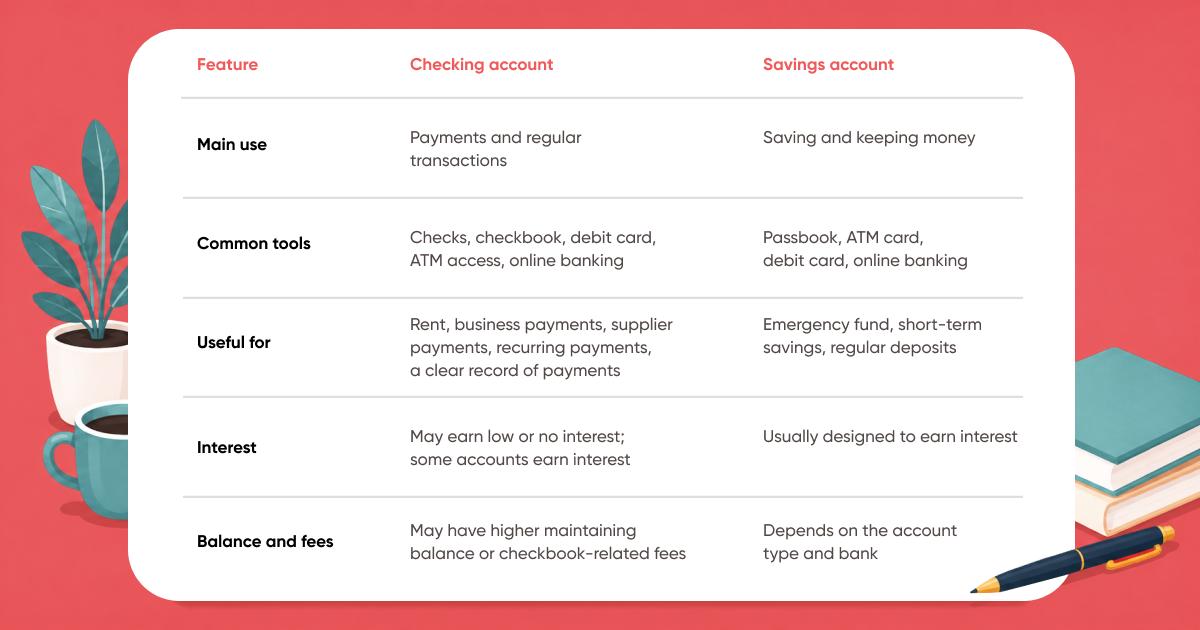

Checking account vs savings account

A checking account and a savings account can both hold money, but they serve different needs.

If your goal is to save, a savings account may be enough. If you need to issue checks or handle regular payments, a checking account may be more useful.

What to consider before opening a checking account

A checking account is worth opening when it solves a real payment need. You may not need one if your payments can already be handled through a savings account, debit card, bank transfer, or e-wallet.

Use these points before applying:

Purpose. Make sure you need checks or checking account features for specific payments.

Maintaining balance. Know how much you need to keep in the account and how the bank computes it.

Fees. Ask about checkbook fees, below-balance fees, stop payment fees, transfer fees, and dormancy fees.

Access. Check if you can use a debit card, ATM, online banking, bank transfer, or branch service.

Requirements. Confirm the latest documents before visiting a branch or starting an online application.

Support. Choose a bank that gives help when something goes wrong, such as unfamiliar transactions, lost checkbooks, or returned checks.

The lowest maintaining balance should not be the only thing you check. Choose an account that fits how you plan to use it.

Open a Salmon Checking account for planned payments. Use it for check-based payments and clear records, with no maintenance fee. Open an account

Frequently asked questions (FAQs)

What does checking account mean?

A checking account is a bank account used mainly for payments and withdrawals. It lets you access your money through checks, debit card transactions, ATM withdrawals, transfers, or other payment options your bank offers.

How do checking accounts work?

Money goes into your account through deposits or transfers, and goes out when you write checks, withdraw cash, use a debit card, or make payments. The bank keeps a record of all these transactions in your account history.

Is a checking account a bank account?

Yes, a checking account is one type of bank account but is mainly used for payments, checks, withdrawals, and transfers.

Can I open a checking account online?

Yes, some banks let you start your application online, but the full process depends on the bank. You may need to submit documents, complete identity checks, provide signatures, make an initial deposit, or visit a branch.

Do checking accounts earn interest?

Yes, some checking accounts earn interest, but many earn little or none. An interest checking account may require a higher balance or specific conditions. Check your bank’s current terms before opening one.

What is the maintaining balance for my checking account?

The maintaining balance for your checking account is the minimum amount your bank expects you to keep in the account. The exact amount depends on the bank and account type. If your balance falls below the requirement, the bank may charge a fee.

29.06.2026